Open test account at a neo-bank in Germany?

The classic division into branch bank and direct bank has been supplemented by “Fintechs” in the past years – technology-driven startups in the financial industry. Not everything that customers won, was a bank, although banking services have been offered.

One just made use of a “nameless” bank in the background. In the front, there was and is a functional and fresh app:

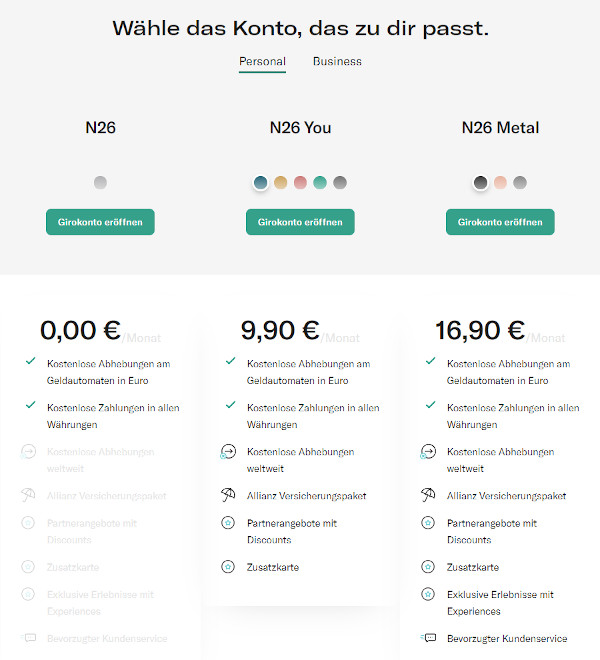

The basic version is free including Apple-Pay and Google-Pay. Further information and account opening ► https://n26.com/.

In the meantime, some Fintechs have again disappeared from the market – others have gotten themselves a banking licence and since then, they appear as “neo-banks”.

Are neo-banks an alternative for us customers and competitors for established branch banks?

In both cases, the answer is:

Not really, but!

First our opinion:

Neo-banks, Germany’s leading one is N26, cannot replace our dear habits and needs in very many cases.

However, they offer a highly interesting supplement to the consisting banking services, such as at N26 for example withdrawing cash free of charge three times per month – no matter at which AMT and of course, without foreign currency surcharge.

The basic version is free of charge. Further services, such as a card made of metal, insurance package or preferred customer service, can be added paying a monthly fee ► https://n26.com/.

The unloved surcharge for payments in other currencies is generally cancelled.

The card and the account can additionally be managed comfortably through the app. If desired, you are notified of what takes place in real time, and you can block the card temporarily or for certain functions.

Notifications in real time on the Smartphone

My test account at the Volksbank and Raiffeisenbank cannot do that. Probably also only the fewest Sparkasse banks.

Therefore the recommendation:

Let yourself be set up with a free test account at a neo-bank and try it!

Neo-banks cannot completely replace our current account, because the accounts were developed for the lucrative standard case and could not yet establish particularities, like joint accounts or authorized persons.

Frequently also the customer service is lacking quality. At N26 in the free variant, this is only reachable through the chat within the app and does not always react very professionally as you would expect from a bank.

But the experience has shown that the expectations in our community towards a free account with great features permits lacking quality of the customer services. This is more tolerated as at a bank where you have to pay monthly for this service!

Positive conclusion for N26 as a secondary account

Who are the true winners among the banks?

It is the direct banks DKB and ING. Also the Comdirect with a top current account, which is now cancelled by the Commerzbank, what many in our community regret and this has already been cause for protest. However, it won’t change anything. Me, being the owner, would not let the customers dictate me how to design my products either.

So, one can assume an intensification of account switchers to the DKB and ING. Now additionally from the storage of the Comdirect/Commerzbank.

The account switch is concentrated towards DKB/ING

Up to now, the local banks, such as the Sparkasse and Volksbank, have lost simultaneously during the cancelling or merging of branch offices.

Why are the DKB and ING the winners?

They can replace almost everthing offered by a tranditional bank, except for the branch office, and sometimes even more. Their accounts are possible in different combinations and in contrast to the locally-bound banks, their current accounts are free of charge without conditions.

Big plus: customer service by phone and e-mail!

Yes, the DKB as well as the ING had problems with the availability for some time last year during the PSD2-switch (Payment Service Directive 2) and also due to the increasing customer rush.

Fortunately, this has normalized now, so that the waiting times have become bearable again. For example, the DKB has hired about 180 new staff members in the past 18 months and has expanded its technical capacities.

Moreover, the customer service works around the clock – also on weekends and holidays. One cannot say the same about the Sparkasse and Volksbank.

However, a good customer service is hardly a reason for opening an account at a bank. It is the conditions and these are by far better at our direct banks:

DKB |

ING |

|

|---|---|---|

| Account management | without conditions free of charge | |

| Withdrawing cash (Germany + Euro-area) |

free of charge at every ATM using the Visa Card |

|

| Withdrawing cash (abroad outside the Euro-area) |

free of charge at every ATM using the Visa Card |

without withdrawal fee but with 1.75 % foreign currency surcharge |

| Cards |  1 Visa Card free of charge  1 Girocard (V Pay), free of charge |

1 Visa Card free of charge  1 Girocard (Maestro), free of charge |

| Start account opening |  (read further information) |

(read further information) |

I have recommended you above to open a test account at a neo-bank like N26 for reasons of trying and supplementing. Have fun “playing” with the newest developments in the banking industry.

Opening an account at the DKB and ING is a very serious thing.

In the past years, many people switched to these two banks and have abandoned their main bank accounts on site after some time.

I have received very many feedback e-mails with “thank you greetings” by people, who are very happy to have taken this step.

Frequent reasons for cancelling the account at the old bank

Besides the worse conditions and worse timely availability of branch banks, a frequent reason for switching was the paternalism by the staff members in branch banks.

Staff members in branch banks often have only a limited financial education, because they are mainly focused on product that they have to sell to customers. Yes, there are still sales plans in banks and the pressure onto the staff to fulfill them, what finally leads to uncomfortable situations and conversations.

A customer only rarely needs the product that a bank currently tries to sell.

Direct banks leave their customers in peace as far as possible. Their staff receives a fixed salary, without raises through provisions at product sales. There are no staff members that should sell you something.

Of course, also a direct bank is happy, if you hold more than only a free current account. The advertising for it has been rather reluctant.

In principle, you should experience good and fast services, so that …

… you have the desire yourself to obtain further bank services of that bank.

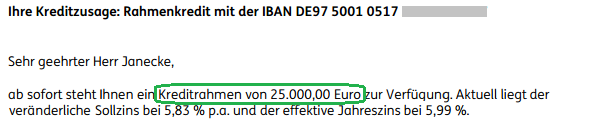

For example, the DKB has an outstanding landlord-package and at the ING, there is the credit line that I myself love so much as my building block for my financial security.

DKB: Main bank on the Internet 😉 with great supplements, such as the ► landlord-package.

We will further inform you this year little by little about the supplements of the free current account through our Sunday Mail.

Excerpt of a letter (PDF) with the approval of Euros 25,000 as a ► flexible credit line.

If you still do not have a current account at a direct bank, …

… then I recommend you to apply for the account opening today in order to implement everything and take more financial responsibility at better conditions.

My current account No. 1:

My reserve current account:

You can get an overdraft facility at the DKB of up to 3-times your incoming salary transfer – at the ING by only submitting the proof of salary payments! You can cleverly create yourself two wonderful and extensively usable new current accounts.

As soon as this is done, you can also try a neo-bank. In Germany, N26 is the absolute leader, even if N26 often has to take some critics– perhaps also because it is so successful.

Germany’s biggest neo-bank:

Are you new to this site?

If I would not have any of these accounts yet, then I would start with the DKB.

Why?

You can find out in one of our next issues.

I had a conversation with directors of the bank this week and I can tell you that what they are preparing lets me count on them.

You could continue reading here:

- Comdirect, DKB or ING?

- Depositing money is free at the ING

- DKB ↝ Withdrawing cash really free of charge?

Leave a Reply