Set up the credit line cleverly ► Part 2

Due to the many replies to the article “How I got a credit line of Euros 25,000”, we have a second part today, with:

- new details and tips

- answers to your important questions

- feedback of granted credit lines

- a link-tip for all trainees/students and self-employed persons among us.

Tip: In 5–10 minutes, you know to what amount you can expect to get a credit line ► www.ing-diba.de/rahmenkredit

Through the information of this article, the probability to get a credit line granted – of exactly the right amount – will increase enormously!

A) Details and tips

A.1 Optimal amount of the credit line

My recommendation to you in the first part was: Be brave and apply for the Euros 25,000 immediately (this is the maximum credit line amount). Further I wrote: If the bank trusts less in you, then it will make you a counteroffer.

It also works vice-versa: On the same evening, a reader answered me telling that he applied online for the credit line of Euros 22,000 and the ING-DiBa proposed immediately Euros 25,000 in the automized creditworthiness check.

Tip: Apply for the amount with which you personally feel comfortable. If the bank suggest a higher amount during the application procedure, then you can accept or decline this offer. A nice thing: you see, how the bank evaluates you!

If you decide to take a lower credit line, then you can apply for an increase earliest 6 months afterwards. Then, however, another creditworthiness check is performed. This is the reason why my tip from part 1 still applies: apply for a high amount immediately. You should not just spend it – but it is currently relatively easy to get a high credit line for future times or emergencies.

► Step-by-step through the online application.

A.2 Reference account

If you are not a customer of the ING-DiBa until now, then the reference account – this is the current account where the payment will be made and from which the interest is debited – your completely normal current account.

If you are already a customer of the ING-DiBa, then you can choose the current account of the ING-DiBa as your reference account. This is practical, if you use the Ing-DiBa as your main current account. However, you can state a current account at another bank already during the application procedure.

If you use the ING-DiBa as an outstanding secondary bank, just like me, and have incidently chosen the current account belonging to the bank, then you can change the reference account. For this, you log into the online banking:

One can change the reference account only once every 30 days. This is why I have entered the date of change into my agenda.

One does not have to open a current account at the ING-DiBa in order to get paid the credit line, like a viewer at Youtube assumed.

Tip: State your main current account as your reference account.

B. Answers to your important questions

B.1 If I want to conclude another loan/car leasing contract later on, do I harm myself, if I have such a high credit line?

Fortunately, one can give the all-clear signal!

It is correct that if one takes a new instalment loan – also a leasing contract is some kind of an instalment loan – already existing loans must be stated.

Also when applying for the credit line of the ING-DiBa, one is asked for loans and leasing financings.

Thrilling – and the reason of the solution is herein –: one is not asked for overdraft facilities and possible credit lines of credit cards and therefore, one does not have to state this type of credit line.

What is the crux of the matter herein?

One has to state loans that have a fixed term and a fixed monthly instalment. This usually applies to instalment loans and leasing contracts, but not to current account overdraft facilities, either to the credit card loan. Neither to our credit line.

The credit line is made permanently (no fixed term). There is no fixed instalment. If you do not use the loan, then it does not cost you anything. If you dispose of the money, then the interest exactly calculated to the date will be debited from the current account.

The credit line is to be regarded as an overdraft facility!

B.2 Should I include my partner as the second borrower?

In fact, this is what the ING-DiBa recommends in the online application. From the perspective of the bank, it is obvious: there will be two persons, who are responsible for a duly loan management.

Also correct is that this increases the chances on an approval of the loan. But the obstacle is indeed quite low (if one does not have problems in the Schufa).

Recommendation: Just enter one person. Perhaps you will want to apply for another credit line with your partner and then you can dispose of Euros 50,000 together!

Only if your first application has been rejected, then apply with the second person. Either you wait 28 days for the new application or you enter the second person as the first borrower and yourself as the second person. This can be done without the 28-days waiting period!

► Step-by-step through the online application.

C. Feedback of the granted credit line

As mentioned further above, a reader was granted immediately Euros 25,000 instead of the applied Euros 22,000. His net income is at about Euros 3,200 per month. There are two children living in the household.

C.1 Does one need such an income to get the full credit line?

As you know from the 1st part, the maximum interest costs per month are at Euros 121.46. To reach this, one has to dispose of the full credit line during the 30 days of the month.

That means: To get the full credit line, one has to have a minimum monthly financial leeway of Euros 121.46 according to the expenditure account (net income minus the limp sums for living, possibly car, etc.) to get the full credit line.

This is why it is not a wonder that another customer also got the Euros 25,000 granted, although he disposes of a net income of “only” Euros 1,700!

Euros 1,700 net income is enough!

(I guess less is also possible)

Just as important as the Euros 121.46 is a good Schufa-score. You know that: banks love to borrow money to people, who have a good creditworthiness.

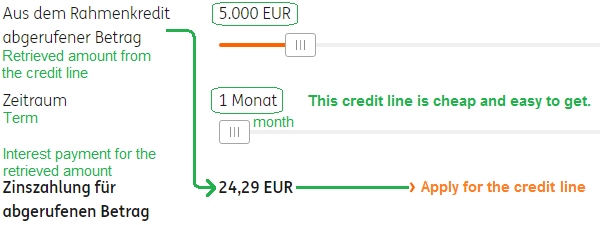

Currently, we do not yet have feedback of readers, who applied for “only” Euros 5,000. If one should use this credit line during the whole month to the full amount, then the interest would be cute Euros 24.29!

Screenshot of the ING-DiBa ► www.ing-diba.de/rahmenkredit

That means that in order to get a credit line of Euros 5,000, you have to have a little more than Euros 25 to freely dispose of!

Attention: At the credit line, we only speak of the payment of interest, not of the repayment. Different from the instalment loan is that there is no repayment plan. If you do not repay the loan, but the interest is debited month after month from your current account, then the bank is pleased. This can go on for years like that! A little caution is indicated, if the general interest level should rise.

Being a smart bank customer, you can see that this is no strategy to build asset. Participants of our Program to financial freedom (German) learn how to get an emergency credit line instead of an almost interest-free call money reserve and to use the generated resources for building asset.

“Start button for the smart credit line”

Prefer to set up an emergency credit line instead of taking true losses of purchasing power of almost interest-free call money reserves!

D. Solution for trainees, students and self-employed persons

The ING-DiBa is, in my opinion, currently the best bank for setting up a (high) credit line. Although, it does not grant this great credit line to trainees, students and self-employed persons.

Inspired by your comments to the first part, I have become active for you and have found a little solution (this is more than participants wrote me, who could not find a credit line for self-employed persons or young people).

“Small” credit line for all professional groups!

The provider that I have found, is relatively new at the market. It is lean and innovative: therefore, there is no field in the online application – which can be completely filled using a Smartphone – which asks for the professional group!

That means: No matter how you earn your money (or whether you even earn money, because there is no field for entering the net income either), you can apply for the credit line!

Of course, there is also a creditworthiness check and this looks like that: Request at the Schufa + one-time online access to your current account in order to evaluate your creditworthiness automatically. Who does not have an online current account or does not want this access, can send the bank statements via e-mail.

At the online access, the loan decision takes place within second, at the e-mail variant, within a banking day.

There is a snag: The credit line is (currently) limited to Euros 1,500.

Further details, the name and the link to the provider can be taken from this overview:

|

|

|

|---|---|---|

| Credit line for smart bank customers | ||

| Term | unlimited (credit line is set up permanently) |

|

| Credit line | Euros 1,500 | Euros 2,500 up to 25,000 |

| Current effective interest rate | 14.99 % (until the 5th of September 2017 and for existing customers: 9.99 %) | 5.99 % |

| Monthly repayment (if money was retrieved) |

5 % of the outstanding amount, at least Euros 20 (until the 5th of September 2017 it was 3%) |

none, only the interest is debited (of course, one can arrange to debit more or deposit by oneself) |

| as a reserve credit line (unused, currently no money retrieval) |

free of charge | |

| Application for … | all professional groups (!) | permanent, no self-employed occupation (workers, employees, officials, pensionists, soldiers and freelancers without business registration) |

| Further information + online application: | www.cashpresso.de | www.ing-diba.de |

| Residence in Austria: At Cashpresso, one can get the credit line also with a place of residence in Austria. Personal note: The elaboration of such articles is a whole lot of work – therefore, I am pleased, if they are used, recommended and linked to a lot. My thanks to you, committed smart bank customer, comes from the bottom of my heart! |

||

You are welcome to post further feedback through the comments feature!

Leave a Reply