Comparison of Current Accounts

Help for using the comparison tool

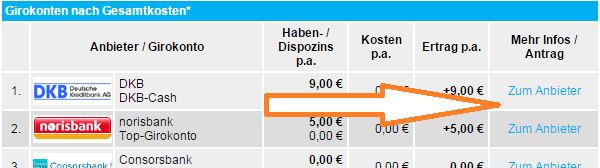

1. Receipt of payment per month

![]()

In Germany, there are few banks that offer their current account (Girokonto) unconditionally free (e.g. DKB and Comdirect). Others, especially if they offer the use of the branches additionally to the online current account, the account is only free from a certain monthly receipt of payment.

Depending on the bank, this is often Euros 1,000, 1,200 or 1,250. Play with the calculator in order to see the differences in comparison. If an account management fee (Kontoführungsgebühr) applies, you can see that in the calculation in the column “Kosten p.a.” (costs per year). The monthly rates were projected to an annual rate.

2. Cards for the current account

![]()

A normal bank card (debit card) – called “EC-Karte” in the comparison tool – is standard for German bank accounts. Only few banks charge an annual fee for this card.

Besides the EC-card (debit card), the Visa or MasterCard credit card have been established by direct banks (Direktbanken), which have often, but not always, a credit line. In the current account comparison, you will generally find “Kreditkarte” (credit card).

Banks with branch offices often charge fees for a credit card and it is not quite easy to get as a new customer. Here, you can find more details on credit cards in Germany.

3. Special Group

Banks often offer free accounts for pupils, students and trainees and the creditworthiness check is not as severe as for adults. If you belong to this group, then please select this option in the comparison tool.

4. Average Balance in the account

![]()

This data is necessary for the calculation of interest. However, there are not many banks left that pay interest on balances in current accounts. You can see the result of the calculation projected for the year in the column „Haben-/Dispozins p.a.“ (balance/overdraft interest per year).

Please note that for a precise calculation at point 6 in the comparison, the days with balance in the account have to be stated for each month.

This calculation could be interesting, if you have a residence abroad in the EU-area and if you are classified as a “non-resident taxpayer” (Steuerausländer) in Germany. Within the European Union, banks are required to report interest income in the following year to the central tax control authority of the country of the bank customer because of the EU Savings Directive (EU-Zinsrichtlinie). If no interest arises, then there will be no report of interest …

5. Average Deficit in the Account

![]()

The comparison calculator assumes that you will obtain an overdraft facility (Dispositionskredit) by the bank for the current account and calculates the interest paid on overdraft.

Most banks have as a prerequisite a receipt of payment for granting the overdraft facility. The amount of this credit line is usually 2 to 3 times the monthly salary.

Some direct banks grant this type of loan on the current account without receiving payment; this is then usually Euros 100 to 2,000. At a corresponding salary payment, this can be increased of course.

Information on a possible increase of the credit line can be found here: Additional overdraft facility? Instructions here!

The number of days with the average loan use is the result of the days in which no funds were present in the average amount (point 4). The calculation is done per month with 30 days, because the banks also calculate only 360 days instead of 365 days per year.

The costs of the credit use can also be found in the column “Haben-/Dispozins p.a.“ (balance/overdraft interest per year) in line two prefixed with a minus sign. In column “Ertrag p.a.” (annual return), you will find the result, so expected annual revenues or costs of the account. The calculation in the background is: interest on account balances deducting interest paid on used overdraft facility and, if given, deducting account management fees.

6. Days in plus and, if given, in deficit

Here, one states the number of days in which the account is expected to have the average balance (point 4), indicated per month. Automatically, the remaining days are the ones without money in the account.

Final Note

Unfortunately, no further adjustments are possible. The calculation with the conditions of the many banks that are included in the comparison is already complex enough and well-suited for a rough simulation for pre-selecting an appropriate current account.

Comparing current accounts

After you have changed the points 1-6, always click on the button “Girokonten vergleichen” (compare current accounts), to view the new result. You can repeat this calculation as often as you want.

Account opening and further information

If you have decided on a bank or want to find our more, then please click on the link “Zum Anbieter” (go to provider). You will be forwarded automatically to the right page of each bank.

Thank you for using our service!

You are welcome to ask questions about the comparison to our editorial staff through the comments feature.

PS: The comparison always shows the top 10 accounts according to your adjustments. However, there are more banks in the database. You are able to see that if you change your adjustments considerably …

Hallo Tanja,

I am an American and I live in the U.S. I would like to open a bank account in Germany because I am planning to move to Germany in the future. As you know, the U.S. has enacted laws (Foreign Account Tax Compliance Act or FATCA) that force foreign banks to collect data on Americans and transmit the data to the Internal Revenue Service (IRS). Many foreign banks simply refuse to accept Americans as customers. So given that I don’t live in Germany and the American laws, will I be able to open a bank account in Germany?

The challenge of the account opening on the part of German banks is the legitimating. According to our German money laundering law, the identity of the bank customers must be determined beyond any doubt.

Some German banks already offer the legitimating through a video call, however, a passport from Germany, Austria or Switzerland is required for this.

Possibly, this will also work with US passports in the future. Our current recommendation is: open your bank account on your next stay in Germany.

The opening of a current account or savings account for US citizens is not a problem at most German banks. However, the opening of a securities account is currently almost impossible.

Your questions about how to select the appropriate account are welcome anytime.

Thanks Tanja. I will try to open a bank account when I visit Germany. The problem is that I don’t live in Germany and I am still learning German. Will I be required to produce other documents in addition to my US passport? My friends in Berlin indicated I should try PostIdent or a notary at Comdirect.

The Comdirect Bank is a very good bank in Germany. It is a great recommendation of your friend!

In fact, the Comdirect accepts an identity confirmation of a US notary. The challenge is that the bank agrees to the account opening.

Before the current account will be opened, the Comdirect performs a creditworthiness check through the Schufa-database (similar to the Credit History in the USA). I guess that only few data about you, or none at all, is saved there …

However, you could open a call money account (savings account) as a first step. There is no creditworthiness check, as you only deposit money and the bank does not have to approve a credit line.

As soon as a customer relationship is established and you have already deposited money, you can apply for a current account opening. Just recently, I have published an article about this: https://www.deutscheskonto.org/en/account-opening-in-germany-from-kuwait/

Would you like to try this? Please let me know of the outcome!

If it does not work, we will find a great account for you as soon as you are in Germany. For this, you will only need your passport and an address – it can also be a c/o-address in Germany – to which the bank can send the bank card and access data for the online banking.

I’ve just published a new article for opening an account from abroad at Comdirect Bank. Currently available only in the German version.

https://www.deutscheskonto.org/de/comdirect-girokonto-eroeffnen/

(translation follows)

Hi Tanja

I am an Australian but have had a basic account with DB for many years. I opened it on a visit to Germany.

I was provided a standard ATM card and Internet Banking access which was all I needed. I recently moved, but when I tried to update my address via the website, it refused, saying that I must provide a German address now.

As a non German citizen or resident, do you believe I will now be forced to close my account?

Many thanks

Ben.

At the DKB – our top recommendation – a change of address to a residence abroad is possible within 30 seconds using online banking . In the case of the Deutsche Bank, I do not have any information.

However, I would simply contact the customer service of the bank and ask to update your address.

A foreign place of residence is still perfectly fine for the Deutsche Bank. In any case, you will be able to keep your account!

You’ve done some great work on this site, congrats.

Would you possibly consider providing a comparison of savings accounts options, to help us choose where to save funds we don’t need at the moment? Obviously I’m not talking about risky investments, but risk-free savings options such as Tagesgeldkonto.

Yes, good idea. Have a look here, please, that should give you an overview: https://www.deutscheskonto.org/en/account/savings/tagesgeld/comparison/

is openbank a good bank?