Secret advice: Car loan in Germany

Besides investment banking (which also bears risks), banks earn most of their money through granting loans. Of course, because they get interest from money, which has been “drawn” with the loan approval.

Guiding idea: Being smart bank customers, we won’t change the bank system, but we know or learn to use it cleverly!

Who knows the banking world a little, knows that there are different interest rates for different loan types. Since shortly, we presented the trick with the cheap installment loan through the form of a housing loan.

Details about the assignment and as a proof in the article!

Today, you learn about an idea of getting a cheap interest rate through a car loan.

Warning

The here presented strategies and ways don’t work with every bank. They are generally applicable. In the course of the article, there will be providers mentioned, where you can implement the strategies!

Background of the car loan

Car loans are more profitable than untied installment loans, because they statistically have a lower failure rate and the loan amounts are higher. Therefore, car loans can be offered cheaper than normal installment loans … because the business with car financing is more requested, there is a higher amount of competitors among the providers.

For us bank customers, it is good, because we have to pay less interest and possibly even further advantages, just like e.g. generosity for the use of the subordinated loan amount.

Especially for people who want to use the purchase of a car to get a high loan amount that it is also sufficient for other desired financing, cannot choose the classic car financing of the manufacturer or the merchant. In this case, the purchase price is known and there are still a lot of banks that want to get the original car licence (formerly “Kfz-Brief” registration certificate). Moreover, the loan contract must be submitted through the car dealer.

In car-dealer-tied loans, the conditions that are less obvious are not that advantageous for you. Their interest rates – where you often look first (and often only at this single rate) – is also very attractive.

Please take a detailed look at the following strategy before you start with the implementation.

Strategy: Using the car loan for bigger purchases

Let’s assume that you find a bank that offers the following conditions independently from the car brand for new and used cars:

- 2.99 % effective and fixed annual percentage rate

- flexible loan payment (3 days up to 3 months depending on the client’s desires)

- car licence does not have to be deposited at the bank

- “additional” applied loan amount can be used freely

- fee-free special repayments possible anytime

- easy online application + easy online processing.

There is such a bank. It is the ► ING-DiBa.

Example of a car loan of the ING-DiBa:

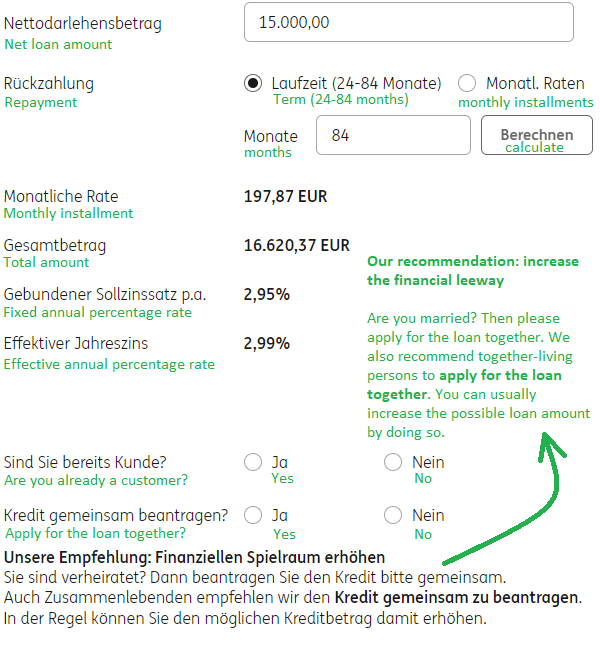

For less than Euros 200 per month, you currently get a loan amount of Euros 15,000 – repayable within 7 years.

Is it meaningful to choose a long term?

Yes, because:

- You can voluntarily repay anytime thanks to special repayments, also comfortably through a standing order,

- You have a higher probability on loan approval, because your monthly installment (burden) is less,

- You can get a higher amount easier (and use it for other financing purposes especially cheaply).

Ready to start?

The ING-DiBa is a great bank, which we permanently observe since years and of which we already presented a lot of other products. Readers, who become customers of the ING-DiBa through us, can look forward to exchange tips and experiences and get help in our community.

But only apply for the car loan at the ING-DiBa, if you know that you have a pretty good credtiworthiness (good income, good Schufa-score). For everyone else and people, who are not sure about that, will find another alternative in the further course (how to get a loan at the ING-DiBa too – a little detour with more security).

Upfront the question of the proof and the possibility of a free use of the car loan …

Correct application and free use

1. Research of the purchase price

How much does you new car cost?

Let’s assume that the car will cost about Euros 10,000. Then it is meaningful to apply for a loan amount of Euros 15,000 because

- one can always take less money than granted (an increase of the already granted loan amount always requires a new loan evaluation and implies additional work for you and the bank),

- You can freely use the remaining Euros 5,000, because the main loan purpose is the car purchase (you won’t get such a cheap loan at any bank).

What type of proof has to be presented?

Within 4 weeks after the loan payment, a copy of the sales contract must be submitted. One can do this through the document-upload in the online banking or send it as an e-mail attachment.

The sales contract is not tied to a special form. A sales contract between private persons is just as valid as a bill from the car merchant. The sales contract must include the following data: seller, buyer, sales item (car), price, date.

If these thoughts (not the implementation) are finished, you can proceed with Step 2.

2. Apply online for the car loan

Open the ► loan application of the ING-DiBa online and start filling it:

Questions on the loan application are gladly answered through the comments feature.

If you do not have your desired car yet, then do not state the payment date. That means that your loan will be reserved for you (without commitment interest) from the approval date 3 months. Only after the payment date, interest applies. But by having the loan approval already, you can start your car search with peace of mind.

At the end of the online loan application, you immediately receive the result of the pre-evaluation. If it is “green”, you print the loan contract, sign it and send it together with the proof of income (copies of the last three salary slips, copy of the remuneration, last tax bill or last pension slip – depending on what applies to you).

If the pre-evaluation is not positive, you take the detour with the alternative. It can be that you get the car loan of the ING-DiBa through this way despite the previous rejection, as it has already happened to one of our frequent readers.

3. Choose and buy the car

With the loan approval, you can start the car search and sign the sales contract with peace of mind.

As soon as this is done, you let the complete loan amount be paid to you. The bank always pays the full amount. You transfer the part for the car dealer and you can do whatever you want with the other part of the loan amount. This can be e.g. the immediate special repayment. With this, you save yourself some months of installment. The installments will not be lowered, but the number of months will be less.

Or you use the money for something else. Important is that you send or upload the copy of the sales contract within 4 weeks to the bank to confirm that the main purpose of the loan was the purchase of a car.

Does it always turn out well?

Yes, in most cases. In the worst case, if you do not provide proof within 4 weeks or the car purchase was only a fraction of the loan amount, the loan will remain active, but the interest rate of the normal installment loan will be charged. This is currently 3.79 % annual percentage rate.

Are you ready for the car loan of the ING-DiBa?

Questions on the application or sequence?

As usually, we and smart people of our community are pleased to help through the comments feature 🙂 Many thanks to our helpers!

The fastest feedback from our community:

Many thanks to Steffi, who was the first person answering to our internal request 🙂 Further feedback is welcome through the comments feature. Thanks!

Secret advice: Subsequent Car Loan!

Perhaps you already have paid a car in cash or with other financing in the past three months. You have done well and correctly. You do not need to get annoyed now, because you can apply for the car loan subsequently and can use the money freely at the super-cheap interest rate of currently 2.99 %.

The application procedure is exactly as described above, only that you add the copy of the sales contract already at the submitting of the loan contract. This applies to all types of vehicles!

Please give me feedback through the comments feature, if you implement this idea. 🙂 Thank you!

Alternative to the ING-DiBa (with higher success chances)

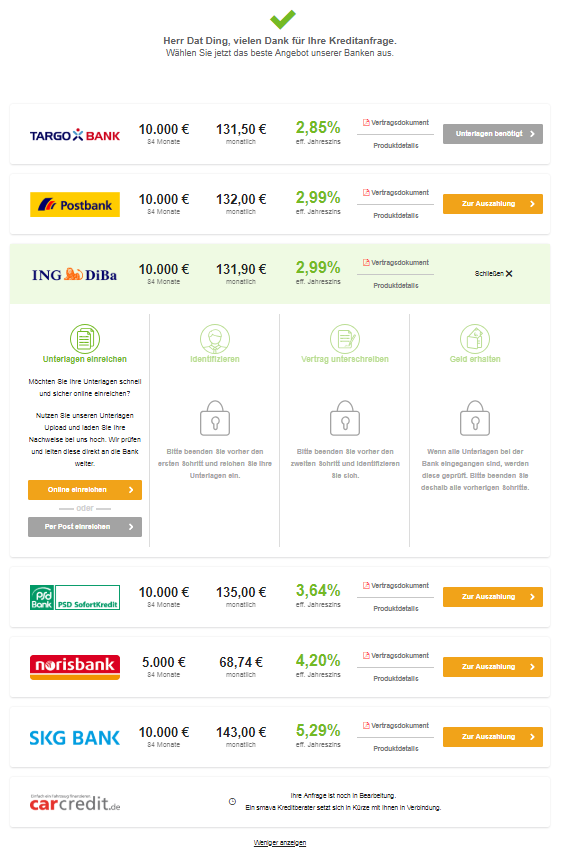

There are two possibilities to get the car loan at the ING-DiBa:

- directly through the yellow buttons above or

- throught the here embedded loan comparison especially for car loans.

Even I, being an existing customer of the ING-DiBa, would take the detour through this loan comparison, because after the comparison, I get several offers by entering the data only once and can choose to my heart’s content.

Entering data once, but several loan approvals for choice!

If the ING-DiBa is among them, I would probably choose it, because I already know the bank and have made good experiences.

If it does not appear in the suggested list after entering the personal data – there will be a creditworthiness check – then I know that it would have rejected me. So I would be glad to be able to choose from other offers.

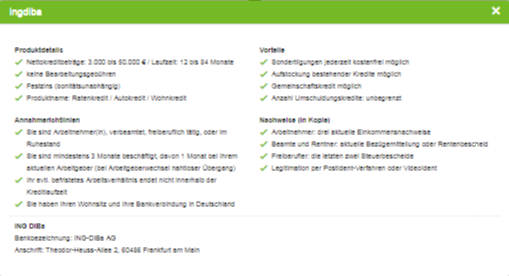

At a small difference of interest, I would choose the ING-DiBa anyway, because I really like the “smooth” conditions. In the listing of the loan partners, you can see all the additional information, if you click on the link “Produktdetails” (product details).

Start the ► comparison now!

This is how the details look like, if you let them be shown through Smava.

As the creditworthiness is checked anyway with the entering of data, it can be that it will be cheaper

with a provider that offers creditworthiness-dependent interest. I can see that in the suggested list. If it is so, then you also have to check whether the other conditions are just as comfortable, such as the special repayments and the free use of the additional loan amount.

Positive experience!

I know at least of one frequent reader that he was rejected by the ING-DiBa at first, when he used the direct way. Afterwards, he used the loan comparison and was shown the ING-DiBa in the suggested list, which then accepted him as a loan customer due to the application through the comparison.

The background is that the loan comparison of Smava that is embedded into our page is attended and due to their years-long cooperations with very many good banks, they know which customers fit to which bank. This is done highly professionally and I am glad that one can become a customer of the ING-DiBa or is suggested another outstanding bank through this way – with loan approval.

Of course, Smava cannot fulfill wonders. However, their success rate is about 50 per cent, which is considerably beyond the average of the industry.

Which variant will you choose?

I am looking forward to an exchange through the comments feature. This is often very inspiring and honestly, this article has been created due to one of these conversations through the comments feature. A heartly thanks to all smart and committed bank customers of this portal!

Further smart loan articles:

- Apply for a flexible credit line up to Euros 25,000 instead of an installment loan

- How to apply for a loan at the DKB

- Get a loan in Germany > without < bank!

Hello, My wife and I moved to Germany six months ago. She works for a German company and we have resident permits and monthly salary payments to a DE bank.

After reading your recommendation about using ING-DiBa for a car loan, used car, I have few questions about the process.

1. We do not have any credit history in Germany. Is that a problem?

2. I am not currently working. You recommended applying jointly. Since I don’t have a job, is still recommended?

3. Is the loan contract available in English?

4. One more question about the buying process. Typically how long does it take to “driving” the car off the lot after finding the right car?

Thanks

Welcome to Germany! Here are the answers for you:

1. Apply online for the loan and see what will happen. Nobody can know the result beforehand.

2. When somebody is not currently getting a salary, it does not make any sense to include them in the loan application as a second borrower. Suggestion: Do the application with just one borrower (the one who is employed)

3. The language for the bank’s contract and communication is German.

4. Hey, we are experts on banking, but not on cars! … Best of luck for the new car.