Best credit line: Ensure it now!

The article Credit line – how I got Euros 25,000 immediately and you can get it too became legendary in the meantime and, if you do not know it already, it is absolutely a reading recommendation.

The credit line exists up to this date, I love it and report about my experiences with it in this article.

In this article, I share my experiences with the credit line with you and you get two variants of a “plan B”. Depending on how much time you have left!

Why do I publish the revival today?

Because people are writing me continuously or have found out during the consultation that they possibly would have gotten it, if they would have made the application when I wrote the article.

Note:

Set up a big credit line, when you do not need it!

Advantages of a credit line

- The setup of a credit line is completely free of charge and non-bindingly (for you, not for the bank!).

- A credit line is like an overdraft facility without current account – only that the credit line is bigger and the interest rate is cheaper for the bank customer.

- With a credit line, you receive a considerably higher loan amount as with an instalment loan.

- The credit line has improved my Schufa-score.

The latter happened to me personally, but it is not guaranteed for you. Even if we were able to determine occassionally that the Schufa-score increased when taking a loan, we would not want to take it for a reason for setting up a loan. The calculation methods of the Schufa are a book with seven seals.

The other three points apply objectively: no costs for setting up the credit line. Only when it is used, moderate interest is charged. It is cheaper than usual for current accounts and the line is higher!

My experiences with the credit line

I follow up with the setup of credit lines since the year 2010. Back then I managed to build credit lines with a total amount of more than Euros 100,000.

Some of them still exist – others do not. I have cancelled some, others were cancelled by the bank.

This is a very important point that is overlooked in many other comparisons!

Cancellation of the credit line by the bank?

You usually do not speak about it online, because you assume that the customer applies for the credit line in the moment of need.

Especially people, who want to live interest-cheaply beyond their conditions, think that a credit line is a good possibility for them and a profitable business for the bank. In the end, it gets interest on money, which has been created mainly by calling the credit line (money creation in the loan system).

For the sake of completeness: By repaying the loan, the created money disappears again. However, this is not the subject of this article, neither the application for a credit line to finance the life standard.

Smart bank customers set up a big credit line in order to be able to react flexibly.

This means: We apply for the credit line at a point of time when we do not need it. Although we do plan to use it in the future, but not even this has to happen!

However, it does not fit into our strategy, if the provider cancels the credit line due to non-use. That happened to me personally at one of the providers.

I cannot speak for all banks at the market, but I know from my own and family experience as well as intensive research that two providers do not do this. One of them is the Volkswagenbank and the other one the ING, my personal favourite provider and top-recommendation.

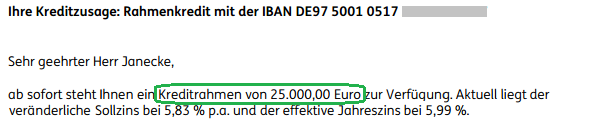

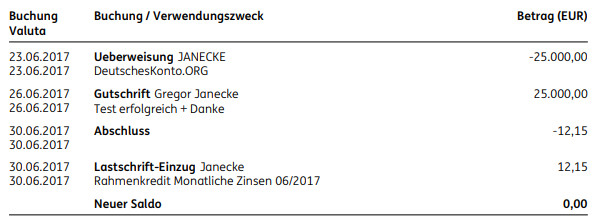

When I applied for my own credit line in the amount of Euros 25,000 in the year 2017 and got it immediately at my disposal, I tested it. I paid the total amount to my current account once and after the weekend, I transferred the same amount back to it:

As you can see on the bank statement, the test cost me Euros 12.15. “A lot”, you might say? Wouldn’t you say it is worth it? I recommend to everyone to test the procedures and please also let the bank earn something someday.

This is the interest for 3 days:

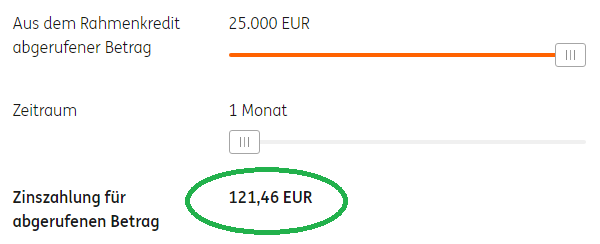

This sums up to a month:

Euros 121.46 is the maximum interest payment. But only if you use the credit line for the whole time and to its entire amount.

If you use a loan of e.g. Euros 500 for 10 days, then you only pay Euro 0.81 for it!

If you do not use the credit line at all, then …

… it is free!

I have done so for about three quarters of a year. That looks like this on the bank statement, which is sent to your electronic post box every three months:

That is how the bank statement looks like, if you do not use the credit line.

Taking advantage of an extraordinary purchase possibility

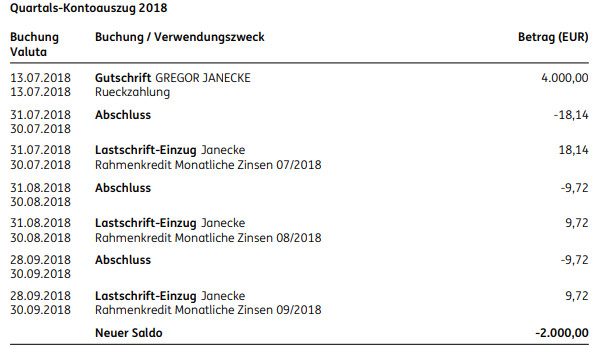

In the year 2018, I had the chance of buying an asset of a five-digit amount. I did not want to touch my securities depots (Keyword: slaughtering the golden goose). Therefore I decided to use my credit line. Bank statement from the third quarter of 2018:

The interest looks quite favourable at a partial use, doesn’t it?

The true beauty of the ING credit line

Only the interest is debited monthly from the current account. The repayment is entirely up to you. This makes it very flexible (most of the other providers stipulate a percentual repayment!)

Use of the credit line in this year?

I have not used the credit line at all this year :

The last transactions were the repayment of the last Euros 2,000 on the 4th of October 2018 and the debit of the monthly interest of Euros 1.30 (not shown here).

However, I could dispose of the Euros 25,000 or a part of it at any time!

And what does the credit line cost me now?

Nothing!

I am truly thankful to the ING for providing this absolutely great and super-fair financial product.

A credit line worth of recommending!

How did you use your credit line until now?

I know from some of our fans that they have got the credit line of the ING in the year 2017 too. How were their experiences in the meantime?

Did you use the credit line and if yes, for what purpose? Have you repaid it already or have you rescheduled another loan with it with long-term?

I am thrilled to read your feedback through the comments feature and look forward to your commitment, many thanks!

Do you want to apply for a credit line too?

This is my absolute recommendation for you and you can find the button for it here:

Here you can find the article with the step-by-step instruction.

Entrance into indebtedness?

Perhaps you ask yourself why I follow up with credit lines since the year 2010, but have only produced comprehensive instruction articles on DeutschesKonto.ORG since the year 2017.

Answer 1: The fear of people getting into indebtedness has kept me from it for years. Perhaps the recognition that “debt is the other side of balance” had to mature in me. Big private asset has not been created by continuous saving, but through the clever use of borrowed capital.

It is decisive that not taking a loan – whereby is is only about setting up the credit line for many people today –, but what you do with it matters! In this connection also our “smart bank customer mindset” applies, of course.

We use the credit line as an emergency credit line in our account system for financial freedom!

Answer 2: It is not always possible, but I prefer to do own tests (or what we can reach in the family and with the help of our community ) to find out what works best.

I am glad to be able to recommend to you two absolute top-providers, the ING and the VW Bank. I have packed the differences between these two here in an overview for you.

From another bank, I got the information that unused credit lines will be cancelled on the part of the bank, and I have experienced this myself. What is the worth of these credit lines? You are on the winning side with our two favourites!

Even better:

Once applied, you can keep these two credit lines for life.

Please value that!

In our fast living world, many things change – also surprisingly. If you now have a permanent work contract, then it is best to apply for the credit line today. What you already have, you will keep! A professional change of status does not have to be shown to the bank. No anew evaluations take place.

Especially in the current time in which we hear of several thousand fired people at big corporations (the middle class string is only worth a headline for few), it is a good idea to simply make the setup. When the date of job cancellation is already on the payslip, it could be too late!

I am talking from readers and consultation experiences. People have wrote me telling about having left their job a few months ago in order to do something else and now they are looking for a credit (line). This is too late. It is best to use ones creditworthiness when it is at its highest point, and this is in a job in which you are working since at least 6 months.

Additionally, the bank currently likes to give away this type of loan.

Get started:

What happens after the online application?

-

In the best of cases, you receive a provisional loan approval immediately online. Then you print the loan agreement, sign it, send it with the PostIdent free of charge to the ING bank or use the comfortable legitimating through video chat.

-

If your application should not be approved, you have two options:

- You take my recommendation No. 2 ► VW FS credit line (works sometimes, if you were rejected by the ING) or

- You become a customer at the ING with a different product first and then you build your bank-internal creditworthiness points. How you can become a customer guaranteed, you can learn in this article..

Questions?

…are welcome through the comments feature at the end of this page. I am also looking forward to your feedback and experiences. A heartly thanks!

Already read?

- 5 credit lines that you can combine wonderfully

- Apply for a credit line through someone else?

- Apply for a credit line up to Euros 5,000

Leave a Reply