Asset building for kids and teenagers in Germany

The asset building for children and teenagers is easy. Especially, if you are a mother or father, as one needs you for the account opening.

Sometimes, the offspring first has to convince the parents to open an account, so that he/she can already start with the asset building in early years.

The most important is the time!

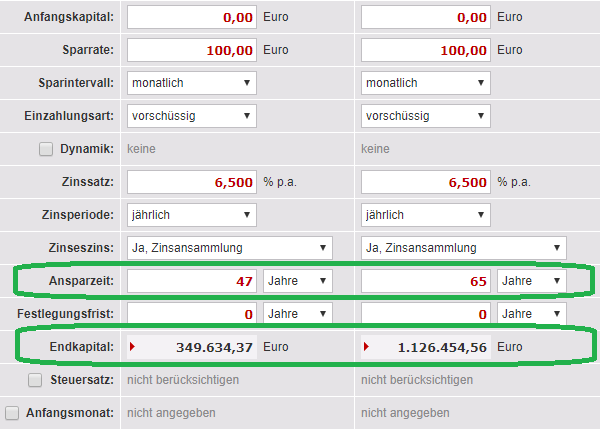

The most important in the asset building is the time. Surely you have heard of the compound interest effect and therefore, the following example calculation will not be new to you:

Let’s assume that you find an investment form that generates on average 6.5 per cent per year – then a baby will become a millionaire until an early retirement age. If you start at the age of majority, it still will be an impressive fortune. But only a fraction of what would be possible! Source: zinsen-berechnen.de

Do you want that your child will be a millionaire?

If you, being a grandmother or grandfather, read this article, then please think of your grandchild. You can bear the savings rate, but mother and father or the legal guardian(s) are necessary for the account opening. More about that further below in the practical implementation part.

What will the decision today imply for your child?

Let’s assume that the asset building starts with the birth and we take again Euros 100 at 6.5 per cent return on investment:

- The child would have around Euros 38,000 at the age of majority and would have an outstanding base for its independent path of life.

- If it would continue the savings rates from the 18th birthday, then it would become a millionaire before the legal retirement age.

- Even if no further deposits took place after the 18th birthday, but the asset would not be touched either, then a final capital of almost Euros 600,000 would be calculated, given a consisting return rate.

Do you wish that your parents would have done this for you?

Yes, I would have wanted that from my parents. My parents have set up a safe savings book with low interest for me and I was able to get a few hundred Euros (German Mark at this time) at my 18th birthday. Okay, my parents were no financial experts, but have done well in a lot of other things.

But with a really good taken decision, the setup and letting it run automatically, the result would have been another one.

I have build my asset myself during my adulthood.

This is different with my kids.

They were not even 10 days old, when their first investment savings plan was already set up.

As soon as you have the birth certificate in your hands, you can get started. For the depot opening – a savings book with low interest is dismissed for me due to experience – you only need the birth certificate of the child, as well as the ID-cards of the parents or legal guardians. Easy, isn’t it?

What did I do for my children?

Every child of mine has a Junior-Depot at the Comdirect. For me, the Comdirect is the best custodian bank for long-term asset building. I myself have a depot for the long-term asset building since the year 2009.

Are you interested in the concrete implementation?

Step-by-step implementation

1. Opening of the Junior-Depot

Go to this website ► www.comdirect.de/junior-depot and start with the opening procedure by clicking on the button “Jetzt Junior-Depot eröffnen” (open the Junior-Depot now).

Then you enter the personal data of the child, as well as of the mother and father or legal guardian(s).

In the application procedure, you are asked for your previous securities experiences. This is statutory. Make your statements truthfully, even if you do not have made any experiences in the area of securities. In our program for financial freedom you can learn a lot about it. 🙂 Everyone starts at zero sometimes. This is a learning and experience procedure.

If all statements are entered, there are some pages to print and sign. Most parents choose the legitimating through PostIdent. For the legitimating, a copy of the birth certificate or a confirmation of birth is attached to the letter. At best, you send it free of charge with the PostIdent to the bank.

If you are already a Comdirect-customer, then it is enough to attach a handwritten note saying e.g.:

If you have several children, you repeat the complete procedure. Unfortunately, you have to enter all data anew.

A few days later, you receive some letters of the Comdirect with the access data for the Junior-Depot.

2. Setting up savings plans

How to set up a savings plan in the online banking, you can learn through this instruction using the example of the Berkshire Hathaway share.

At the Comdirect, you can currently regularly save with 138 single shares from Euros 25. We are working, so that even more shares become available as a savings plan.

If you are not sufficiently versed with single shares, then it perhaps makes sense to set up a funds savings plan or ETF-savings plan so that the asset building takes places parallel in a great number of stock companies. Of course, there are also investment products on commodities and bonds.

If you cannot afford Euros 25 per month, then arrange that the savings plan should be implemented bimonthly or quarterly. That would be Euros 12.50 or 8.33 per month. This can be the case, if you have e.g. several children.

Important is that the asset building is started in the first place!

Financing of a savings plan

There are two possibilities:

- If you set up a standing order to the settlement account of the Junior-Depot, then you can let the savings plan be debited from there (you can give this account number e.g. to the grandparents and they set up a standing order) or

- you arrange to debit the savings plans by direct debit from the parental current account.

In the case of my children, one part is transferred by the grandparents and one part by me to the settlement accounts of the Junior-Depots. The money is debited from there. Simple.

Questions about this subject and on the depot opening are welcome through the comments feature

Investing in what?

You can take this decision yourself! But you can also get inspired by us and other smart bank customers. You can exchange your ideas through the comments feature at the end of this page.

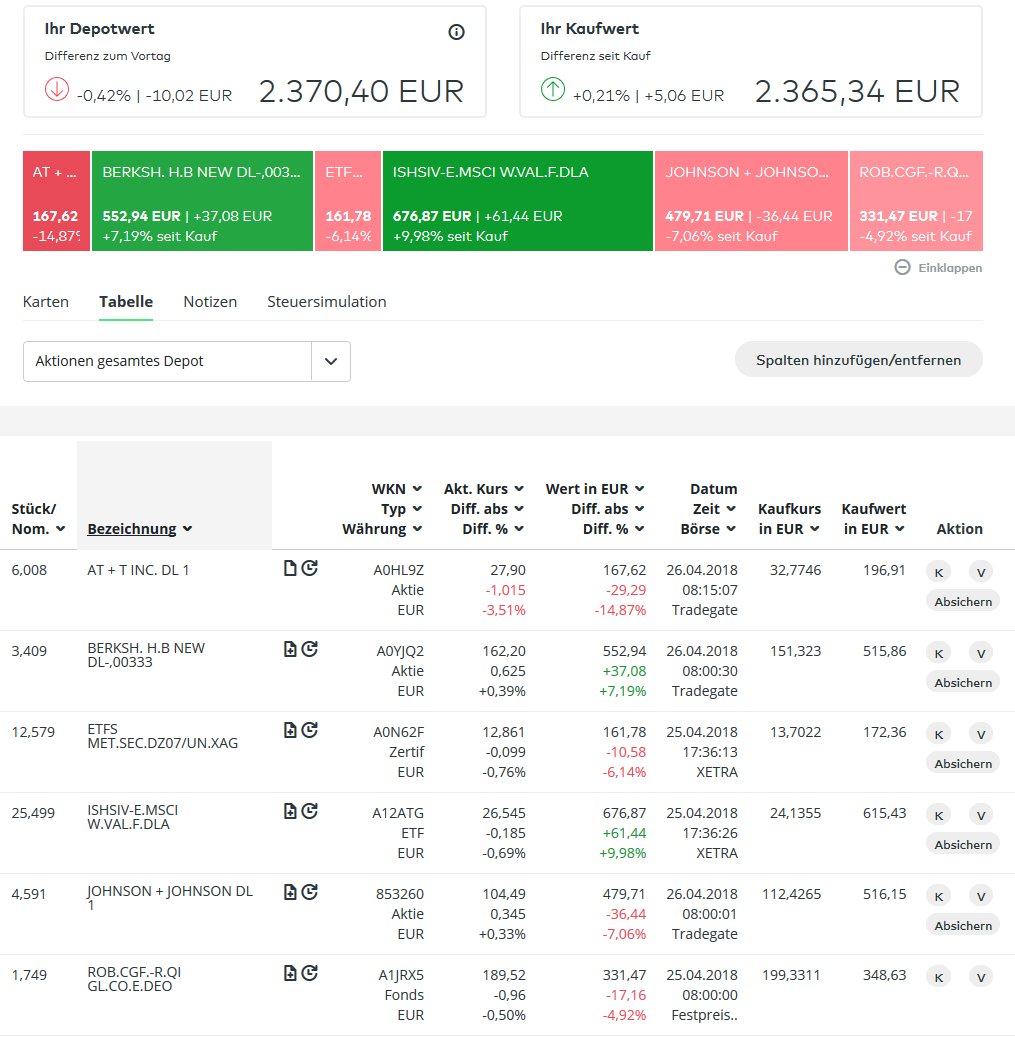

As a stimulation, please take a look at the screenshot of the Junior-Depot of my youngest daughter:

I certainly have not made everthing right, but I do something. One can never be 100% right and I can only see the success at the 18th birthday of my daughter. This here is only a current intermediate result with red and green, depend where you are financially, the Euros 2,300 are not bad for a three-year old girl. In the case of her older siblings, the depots are already in a five-digit area.

You can see that I have decided for a mixture of shares and funds.

Please write for which securities you have decided or would decide for, for me and as an inspiration for future readers.

Moreover, I am interested, whether you have opened a Junior-Depot due to this article or plan to do or have even done it before?

Why do we parents do that? Because we love our children and want that they have it (even) better than we!

This is also the boost which makes our society continuously rise.

Ready for the next step?

Recommended from our own year-long experience!

Supplementing articles:

- Opening of the depot-account for adults (Comdirect)

- Passive income through capital gains

- Current account for 14 to 17-year old teenagers (secret advice)

- For Comdirect-newcomers: 9 reasons for and one against!

Thoughts about the today article in a video:

The recommendation of this article is explicitly welcome 🙂 Thanks!

Leave a Reply