Opening the Junior-account at the DKB?

Who does not know the DKB yet, will be surprised that a bank configurate a junior account so generously:

- account + cards are completely free for children and parents

- free withdrawing of cash within Germany and abroad

- free credit card (Visa card)

- free Girocard (colloquially: EC-card)

- favourable interest on savings balance

- possible for minors between 0 and 18 years

The only requirement:

One parent must be or become a customer of the DKB. If you do not have a free account at the DKB yet, you can change this here: www.dkb.de/kunde-werden.

How the DKB Junior-account works:

Do not want to miss any videos? Youtube-Kanal abonnieren

DKB Cash u18 explained in detail ✔

A) From 0 to 8 years

As you have learned from the video clip, the account may be applied for and opened immediately after the child’s birth. For the legitimating, the birth certificate (Geburtsurkunde) in the original or a duplication of the birth confirmation (Geburtsbescheinigung) is submitted, for example, the one to apply for the child benefit (Kindergeld). You get the birth certificate sent back from the bank by post.

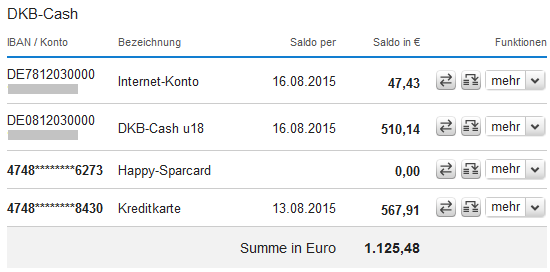

As the baby or the child cannot dispose of a bank account by itself at this age, you will manage everything as a parent(s). Therefore, your DKB-Internet banking will be expanded by two accounts:

- the DKB Cash u18 (current account for minors)

- the credit card account (usually used for Visa-Savings)

The Junior-account at the DKB appears as an addition in the online banking of the parents. In our example, these are line 2 and 3. If both parents are customers of the DKB and both have parental authority, then the u18-account will appear at both.

The Junior-account will be managed through the online banking of the parents.

During this age, mainly the feature Visa-savings is used. The Visa-savings work like a call money account (Tagesgeldkonto).

The only difference is that the money is on the credit card account (Kreditkartenkonto), and in addition to the return transfer, it could be withdrawn with the Visa credit card free of charge at any ATM.

Most parents keep the Visa credit card safe in their bank folder, because it is actually not used, but automatically issued by the bank.

The conditions of Visa-saving

- 0.7% interest on balances up to Euros 300,000 (variable interest rate)

- monthly interest payment (Zinsgutschrift)

- balance is available at anytime (by transfer to the current account or by Visa credit card)

- 100% German deposit protection

Important note

For the savings to earn as much interest as possible, it must be on the Visa credit card – not in the children’s current account, because the balance only receives 0.1% interest there.

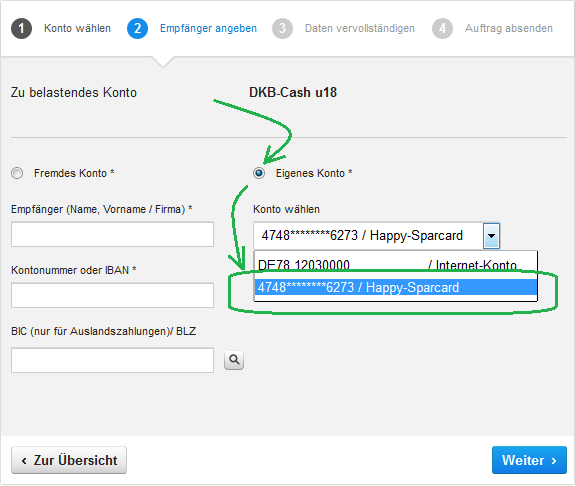

As officially no direct transfers to the credit card are possible and as I want to spare you the regular transfer, I will tell you about a feature that enables you to transfer automatically the balance of the children’s current account to the Visa credit card.

This is meaningful, e.g. if you and/or the grandparents have set up a standing order (Dauerauftrag) to save money for the child:

1. Start a new transfer (Überweisung) from the children’s current account and select eigenes Konto (own account) and then the Visa credit card of the child.

The transfer from the current account to the credit card account is an internal transfer.

2. In the second step, you determine that the transfer should be performed as a monthly standing order (Dauerauftrag) by marking at Ich möchte monatlich das verbleibende Guthaben von dem oben genannten Konto auf meine DKB-VISA-Card überweisen (I want to transfer the remaining balance on a monthly basis from the above mentioned account to my DKB Visa credit card).

With this automated transfer, the current account is cleared every month for the benefit of the savings account. Do you find this practical? This, of course, also works for the adult accounts.

B) From 8 to 14 years

For this age group, all aforementioned applies of course. Additionally, children and teenagers develop their own economic activities at this age. It is a good time to introduce children to bank accounts and bank cards and the dealing with them.

With the DKB Girocard, e.g. own purchases in stores and tickets for public transport can be made.

Recommendation for use: Online account and Girocard

If you are lucky and live near a DKB deposit machine (Einzahlungsautomat) (page in German language), then your child can even deposit cash by itself.

Admittedly: depositing is a small flaw of the DKB account: As the DKB is an Internet bank, it has no branch offices, to which you could carry the piggy bank in order to perform cash deposits.

At the deposit machines, it is only possible to use bills. No coins. And there are only about 15 deposit machines nationwide.

Solution idea:

If your child has been saving money, put it into your wallet and transfer the equivalent to the youth account of your child. Agreed?

C) From 15 to 17 years

During this age, often the need for an own (prepaid) credit card arises … and you have this already since the first day of account opening.

For example, a credit card number is required for online games or Smartphone apps, as well as for other Internet applications or booking of tickets.

Additionally, school trips or student exchanges are on and your child will always have money with the DKB Visa credit card. It can pay comfortably cashless abroad with the card or withdraw as much cash (Bargeld) as needed locally, of course, free of charge and without fees of a possible currency exchange.

DKB Visa credit card is ideal for school trips

If it should not have enough money, you as parents/parent can make a transfer from the current account via online banking, and already at the next day, it can use the new money on the credit card for further use.

However, it does not necessarily need to be a journey. Your child can pay cashless in many shops in Germany or withdraw free cash from ATMs with the Visa credit card.

Tip: Additional Visa credit card to separate saving and spending

Just as with the adults, there is also the possibility at the Junior-account to obtain a second Visa credit card free of charge.

- One card is used to save money (savings account) and

- one card is used for spending.

The separation makes sense, because otherwise, one constantly spends the saved money.

You can find out how to apply for the second Visa credit card here: Get a second credit card.

For 15 to 17-year-old teenagers, the DKB account is ideal. Despite real bank and credit cards, the adolescents cannot become borrowers, because there is no credit line granted – however, they can use all features with their balance.

With the 18th anniversary, the young man/woman takes the account completely. From now on, the DKB makes available a credit line on the current account and the credit card at a corresponding income. One can use it – but does not have to.

Opening and Set up of the Junior-account

The DKB Junior-account (official product name: DKB Cash u18) cannot be applied for separately, but only from an existing account of an adult.

That means in the classical case: mom or dad must be DKB-customer(s).

If you are not yet a customer(s), you can become one at any time (provided a corresponding creditworthiness/no negative Schufa). Perhaps, it is a good idea for you to take advantage of the benefits of the DKB. However, you do not need to do this. You do not have to deposit anything on your account, as it does not cost anything.

Once you are a DKB-customer, you can order further products to your account. The Junior-account is namely a further product.

Log into your online banking and follow the green arrows:

Opening a Junior-account is very easy, if one already is a DKB customer.

If you are already a customer of the DKB, then there is no rejection at the opening of the Junior-account. You can open as many Junior-accounts as you have children. 😉

Guaranteed account opening

At the opening of the Junior-account, both legal guardians must sign the application for account opening and both must be legitimized. One of you is already, as he/she has an account at the DKB. The other one can do this through the PostIdent-procedure or through a Video-Chat. If both parents are already customers of the DKB, the legitimating does not apply anymore.

Note: Only the guardian or the guardians may open the Junior-account in the name of the child. Normally, this is not the grandma, grandpa, aunt, uncle or other related persons. If you are reading this article, perhaps the opening of a DKB account is worth for other reasons?

“Apply for the DKB-Cash now”

What experiences have you made with the Junior-account?

Please take advantage of the opportunity to share your experiences of the Junior-account here with other parents. The comments box is open for this purpose. Feel free to ask questions to the account or its opening and use.

Further popular articles about the DKB account:

- The 11 most important features of the DKB Visa credit card

- DKB Visa credit card Prepaid for minors

- Opening the DKB joint account

Leave a Reply