“Corona-Loan” for private persons

Many of our subscribers of various years have already set up their personal credit line system. The key to it is the 5-credit-lines-system as a supplement to our account system.

Perhaps you are not with us since long or have been guided to our smart bank customer community through a recommendation.

This article shows you how to use your (still) good creditworthiness, in order to …

… get two free credit lines!

The advantages are obvious:

- The setup of both credit lines is absolutely free of charge

You only pay interest, when and if you use the loan and only in the amount and for the time, in which you use it. - You have the “right” to take advantage of the loan …

… but you do not have to! Today, you only apply for the credit line. - Management completely online

That means, you log in and make a transfer or pay with the card using the credit line. A further authorization of a banker is not necessary!

► Omit the background and go immediately to the solution

Background: Facts and the resulting insights

Currently, the situation at the job market and as a consequence of the general creditworthiness level in the country looks rather good.

However, it is no secret anymore, that also banks prepare for turbulent times in autumn.

A bank likes to earn money through granting loans. It evaluates the probability of repayment with the help of a computer. If the computer says the probability is too high that there could be problems with the customer or with the applied for loan, then no loan is granted.

Bank computers have no heart – they calculate with databanks.

At the application for a loan, normally the last 1 to 3 salary slips have to be presented. Do you still have some, on which no short-time work or cancellation date is mentioned? Very good!

The press published different data from 600,000 to 800,000 companies that have registered for short-time work this year. Obviously millions of salary slips are already marked with a reduction of the creditworthiness.

Short-time work is still better than unemployment. With this “status”, the application for a loan will generally not work out.

Therefore, please, – if not already done – do something for you and possibly your family too.

Even if you are a civil servant or earn your money in one of the industries spurred by Corona, please recommend this article to the people in your personal environment.

One point is important for your comprehension:

It is about creating yourself (free) cash reserves. This is related to the motivation of the state for the immediate help during Corona-times. This was not for companies that were broke anyway, but for healthy companies that encountered payment difficulties (cash bottlenecks) due to the Corona-incidents.

Even a private household can have liquidity bottlenecks. For example, because an employer cannot pay the salary even though the employee rendered work performance.

Should you or possibly your kids suffer hunger because of this?

If no savings, such as call money are available, you can “finance” the groceries with the credit line.

You may prefer paying some per cent interest to hunger.

2 solutions for our readers

1. Increase overdraft facility or apply for an additional overdraft facility

Of course, you can apply for an overdraft facility or increase the existing one at your current account holding bank.

Sometimes it is better to have such bank products at a bank that has specialized on such, due to the conditions and/or another type of relationship.

Our frequent readers already know what this is about: The credit line of the ING. Best is to figure it having an overdraft facility at a different bank.

You get:

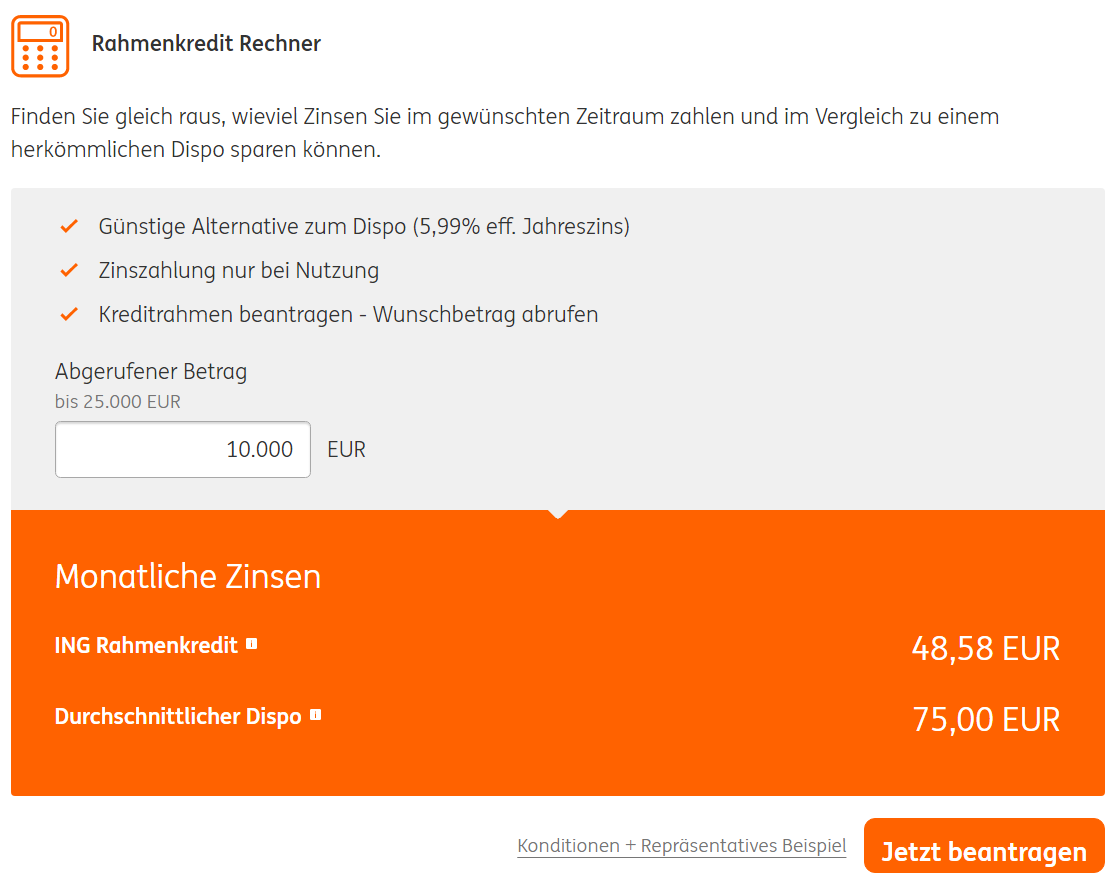

- Depending on the application and approval, a credit line between Euros 2,500 and 25,000.

- You get access data to the online-banking, so that you, whenever you need money, can simply log in and transfer money to your current account.

- You only pay interest for the money you use and for the time you use it. Currently, it is relatively cheap with 5.99% annual percentage rate. The credit line is absolutely free of charge during the time in which you do not use it.

Use it flexibly, no matter what comes:

Divergent from my former recommendation of Euros 25,000 for good earners and Euro 5,000 for lower income earners, I would currently apply for Euros 10,000.

Euros 10,000 currently have a good chance.

There were signs on the part of the ING that this amount currently passes particularly well. You can increase it later on, although there will be another creditworthiness check.

In the current time, it is preferable to have Euros 10,000 in additional overdraft facility than nothing, isn’t it?

I personally have this credit line since some years and am very thankful for this product, which I have occasionally used and then many months not at all.

If you would use the full amount of Euros 10,000 for a month, then there would be an interest of Euros 48.58 according to the current interest rate. The interest rate varies and adapts to the market. ► Start own calculation . ✅

2. Apply for the credit line on the Visa Card or increase it

The same applies here: You can increase your credit line of a consisting credit card – now is perhaps still an acceptable moment. Or you get yourself a new Visa Card without annual fee (= no current costs).

If you can take the hurdle of the application, then the Barclaycard Visa is particularly interesting, because:

- this Visa Card is not only without annual fee – you can also withdraw cash with it free of charge on the part of Barclaycard and the foreign transaction fee (what most credit cards have) does not apply either.

- there are currently Euros 50 initial balance.

- the credit line can be “trained” through its use. This is almost unique at the German market. Here you can find a documentation on how I trained my Barclaycard to Euros 9,500.

You can even pay offline bills using the credit card …

Admittedly, Barclaycard also offers services through which it earns with fees. For example, you can upload a bill within the online banking and Barclaycard makes the payment from your account. You can also transfer money to other accounts. However, this costs Euros 7.50 per procedure. Transfers to your reference account (current account) are free of charge.

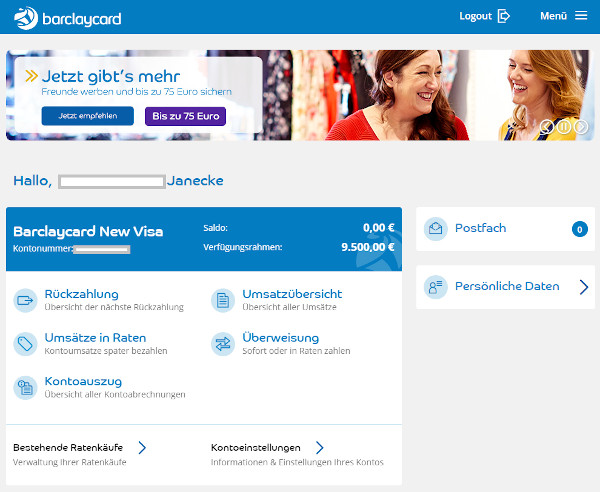

Within the online banking, you have more possibilities than you are used to from other credit cards:

This is a screen shot of my own account. The built credit line is at Euros 9,500 and remains unchanged since years. We have people in our community, who managed to train it even higher. Immediately after the application, I would carefully count with Euros 3,500. Of course, everthing depends on your income and the creditworthiness.

Barclaycard unfortunately has become a little “stricter” when granting this really outstanding credit card, so I would not wait any longer with the application, if I was a “not-yet-customer”! There is nothing to lose – only gains!

Application … preferably today!

► Start the application and get your Euros 50 initial balance ✅

Summary

We do not know, what the future holds, but the signs speak of a turbulent autumn. So let’s take care of our finances in order to be able to dispose of them well in any situation.

Banks, accounts and credit lines should be used smartly and serve people. Please also involve yourself for the people in your environment, no matter if it is your family or a neighbour. Forward the information wherever it is welcome. At doubts simply address the subject first.

About the product ideas: Both suggestions have their advantages. Fortunately, you can combine them very well. With the Barclaycard, you can even get a loan comfortably being at the checkout. You only have to allow the 3.5 per cent of the loan amount to be transferred monthly from your current account. At the credit line of the ING, it is only the interest.

You can repay everything at once too, so that the credit lines are free again.

Use the scope of action, that you can get thanks to these outstanding products, smartly.

Questions? Experiences?

As always, I am looking forward to the exchange with you through the comments feature at the end of this page. Let’s exchange our ideas, tips and experiences for the benefit of the community.

A hearty thanks for the high and smart activity, as well as the help with questions and answers between each other. I also like to contribute with my experience!

Other frequently read articles:

- Loan at short-time work possible?

- Open a Schufa-free current account?

- Open a secondary account abroad

Leave a Reply