Joint account DKB vs. Postbank

Perhaps the subject joint account has been missed out a little on our special portal for smart bank customers. Let’s change that together today!

Many together living persons exploit the practical advantages of a joint account. Both account holders deposit and both have own cards and respectively a separate access to the online banking.

Why shouldn’t you exploit the advantages of the doubled creditworthiness?

German banks are offering special or free services again, if a minimum amount is transferred monthly to the account. Perhaps you like the idea of pooling your monthly incomes in one account in order to get advantages which you alone would not have received?

Comparison: Online versus branch (joint account)

DKB (online bank) |

Postbank (branch bank) |

|

| monthly incoming transfer for the following conditions | Euros 700 | Euros 3,000 |

| … if the minimum amount is not transferred? | Euro 0.00 per month | Euros 9.90 per month |

| Account management fees | Euro 0.00 | Euro 0.00 |

| Girocard per account holder | Euro 0.00 | Euro 0.00 (Postbank Card Gold) |

| VISA Card per account holder | Euro 0.00 | Euro 0.00 |

| Cash supply | ||

| At the counter of the Postbank | no | yes, free of charge |

| AMTs of the Postbank and further CashGroup-banks | yes, free of charge | yes, free of charge |

| At 1,300 Shell-petrol stations within Germany | yes, free of charge | yes, free of charge |

| At about 95 % of all other ATMs within Germany | yes, free of charge | no |

| Withdrawals in the abroad | yes, free of charge | yes, free of charge possibly plus 1.85 % foreign transaction fee |

| Cash deposits | only 16 deposit machines within Germany | every post branch office |

| Service and availability | ||

| Branch office? | no | yes Note the opening hours! |

| Telephone customers service? | yes Mon–Sun around the clock |

yes Mon–Fri 9 am – 6 pm |

| E-mail / letter? | yes | yes |

| Bank statement printer | no | yes, free of charge |

| Limits and interest | ||

| maximum possible amount of overdraft | 3-times the salary transfer | 3-times the salary transfer |

| Overdraft facility-interest rate (within the credit line) | 6.90 % | 8.68 % |

| Overdraft facility-interest rate (tolerated overdraft of the credit line) | 6.90 % | 12.60 % |

| Instalment loan-interest rate | 3.49 % (creditworthiness-independent) |

2.47% – 9.49% (creditworthiness-dependent) |

| Call money-interest rate | 0.20 % | 0.01 % |

| Account opening | ||

| Place of residence | Germany, Austria, Switzerland + German expats | Germany |

| Possibility of account opening | online | online or branch office |

| Apply for the account opening: |  |

|

| This comparison has been consciously created as a joint account, because if two account holders arrange to transfer their salary or other income to the account, the probability is higher that the Euros 3,000 of minimum incoming transfer is reached at the Postbank. The specifications apply independently from the number of account holders! | ||

Details of the comparison

Money or salary transfer?

The pleasant news at the DKB and Postbank is that they do not turn the salary transfer into a requirement for the fee-free account management, but only the money transfer.

The amount does not have to be transferred at once. It is sufficient, if it is transferred distributed as partial payments in the course of the month.

If one wants to apply for an overdraft facility, then the salary transfer is necessary. For the use as a free secondary account (e.g. joint account as the household account or the residencial community account), the setup of one or several standing orders is enough.

Use as a secondary account possible

Recurrence into the chargeable use?

If the minimum amount is not transferred within one month, then the Postbank charges Euros 9.90 in account management fees.

At the DKB, the account remains free of charge. If the amount is not transferred within the following month – not all employers pay on time every time – then you are changed from the status active customer to the not-very-active-status. However, an account management fee is not charged either. The DKB-account is generally free of charge. But some services are limited or fees are charged for them (e.g. foreign transaction fee). Details about active and non-active customers are summarized here for you.

DKB is always without account management fee!

Deposit cash

Cash deposits happen very rarely for the most private customers, however, we of the editorial are frequently asked about them. Herein, the Postbank is clearly in advantage with its thousands of branch offices. Whoever wants to deposit cash free of charge can visit any branch office of the Postbank during its opening hours.

At some sites, the Postbank offers deposit machines, so that you can deposit bills and at some machines even coins. The DKB also makes deposit machines available to you. However, these are not everywhere in Germany. (List of sites)

Withdraw cash

Even if a fee is displayed at the ATM for the withdrawal, as shown here at the Sparkasse, the withdrawal is free of charge for the DKB-customer. Being a DKB-customer, you quickly get used to the fact of being able to withdraw cash free of charge almost everywhere.

Note: There are some countries, such as the USA, Canada or Thailand that have a different bank structure and where it is common that the withdrawing person has to pay an extra fee for the ATM-use. In this case, either the here presented DKB or Postbank can change that.

At the significantly more often used feature withdraw cash you do not have to worry being a DKB-customer. Around the globe, more than 99 per cent of all Visa-able ATMs are available for your free cash withdrawal.

You can even withdraw cash free of charge at the ATMs of the Postbank. However, this is not possible vice-versa. Conversely, the DKB-customers do not get cash free of charge at the counter of the Postbank. 😉

If one adds the optimal credit card at the Postbank, one can also withdraw cash free of charge abroad. However, 1.85 per cent foreign transaction fee is added outside the Euro-area.

The DKB is better abroad

At the DKB, the credit card payment in a foreign currency as well as the cash withdrawal in other currencies are freed from the foreign transaction fee. Moreover, the Visa Card is included in the standard-equipment of the account.

Additionally at the DKB there is a free emergency help at the loss of the Visa Card (emergency card with express-courier, emergency cash already on the same day). How well that works, I was able to experience already for myself.

Detailed report: How it works in the case of emergency!

Customer service

Experiences with the customer service are often quite individual. You will probably make very good to dispensable experiences with both banks.

As I am an active DKB-customer since 2004, I know the bank already very well. For this article, I was allowed to make a considerably more intense research at the Postbank, which was partially a challenge and which is why this article did not become very extensive.

In contrast to the DKB, the Postbank works with different telephone numbers and partially confusing recorded messages. The telephone service hours are differently stated on the website as well as by the service staff and in the experiment on myself, I faced different availability hours. I does not help at all, if the recorded message tells you to call later again. This is not availability. 😉

Perhaps to blame is the huge number of products at the Postbank that the state of knowledge of the Postbank-employees was not always comprehensive. Even at not really difficult question, one forwarded me to another telephone number. In another case, also a consultation with the team leader did not help; so I was asked to send the question by e-mail. But there are again different e-mail addresses at the Postbank.

The telephone customer-service of the DKB is good within this industry, but not the best either. For us customers, however, there is only one telephone number and only one e-mail address. The DKB offers an around-the-clock-service. This is considered as very pleasant by many customers, as they can clear questions or problems with the bank also after the end of work or on weekends.

Nevertheless, the fact to have the possibility of going into one of the many branch offices speaks in favour of the Postbank!

Who does not want to miss the bank statement printer, opens his/her joint account at the Postbank. At the DKB, there are only online bank statements.

I myself use the bank statements only very rarely. It is enough for me to see the last entries in the transactions overview to see whether everything is okay.

The author on his research trip …

Set up the overdraft facility and credit card

Most customers of the DKB receive an overdraft facility line of Euros 500 already at the day of account opening.

Euros 500 immediate overdraft facility

With this, problems are avoided that could arise if payments overlap. For example, a late money deposit and direct debits, such as energy or telephone bill. Return debit notes cause unwanted consequences and additional work.

At the DKB as well as at the Postbank, the overdraft facility can be increased to up to 3-times the monthly net income at a good creditworthiness and salary transfer. One can apply for it after the transfer of the first salary payments.

Overdraft facility up to 3-times the salary

With the salary transfer, also the limits of the credit cards can be adjusted. If the credit card limit should be too low at first, one can transfer from the current account to the credit card account at both providers and by this increase the overdraft facility.

Important to know: At the joint account, there is a joint overdraft facility and therefore a joint overdraft line. The credit cards are issued personally and for every account holder, there is one credit card account with a separate credit line.

There are possibly even further models at the Postbank. This was a little unclear at the research and partially contradictory.

If your are already a Postbank-customer, I would be glad, if you could supplement this article with your experiences through the comments feature at the end of this page. Many thanks!

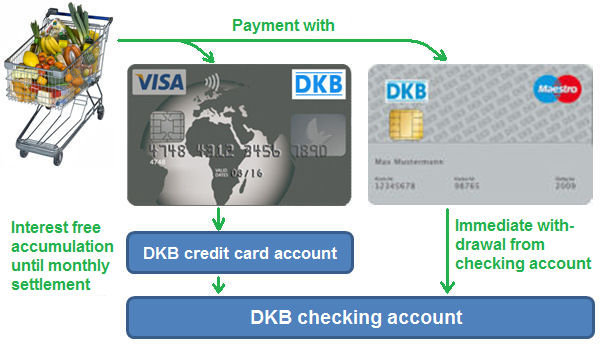

At the DKB, the credit card balance is settled with the current account automatically monthly. Expensive credit card interest can’t ever be charged. If the joint current account has not sufficient balance, then the relatively favourable overdraft interest applies.

Some people prefer the direct debiting from the current account (please use the Girocard for this purpose) and others prefer the gathering on the credit card account with the subsequent settlement (please use the Visa Card for it).

The Postbank offers besides the automatic settlement a credit card loan, which is currently 14.95 per cent and more expensive than the overdraft interest rate and even more expensive as the interest rate for tolerated overdrafts. A “tolerated overdraft” is, when you take more money from the account than the agreed overdraft facility provides. I recommend to avoid that, because the risk of undesired return debit notes or card blockings always exists.

If the expenditures are unexpectedly beyond the limit, it is recommended to briefly “switch” to a cheap credit line or make a planable payment through an instalment loan.

The DKB (www.dkb.de/privatdarlehen) as well as the Postbank (www.postbank.de/privatkredit) have a corresponding offer for this purpose. If you stay at “your” bank, you save yourself from an anew legitimating. Loans are granted independently from each other and both banks work differently: At the DKB, the interest rate is the same for everyone (cheap) and at the Postbank, you pay less interest having a great creditworthiness than the customers with average to bad conditions. You can find out more about the subject debt rescheduling here.

We do not need to talk about the income investments (call money, fixed deposit) because of the current market situation. The conditions have hit rock-bottom. Both banks offer a securities depot, which can be managed together or separated.

Questions and answers about the account opening (joint account)

Can I open a joint account without being married?

Yes, this is possible. You can choose whoever you want as the second account holder (joint account holder). This can be e.g. the flatmate (residential community).

In the online application, the bank does not query the relationship between the account holders.

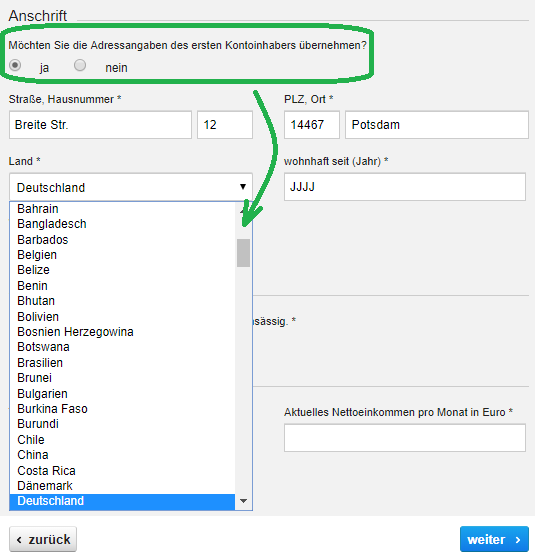

Can I open a joint account with my partner living abroad?

Yes, this is possible at the DKB:

In contrast to many other banks, the joint account at account holders with different addresses is possible at the DKB. Even if the second account holder lives abroad.

Can I convert a single account into a joint account?

This is possible at the Postbank.

A convertion is not possible at the DKB. Please open a new joint account. The existing account can still be used free of charge or cancelled. In the online banking, you would see the joint account and single account together. You have a separate free credit card for the single account, as well as for the joint account. Which one you actually use, is up to you.

Does the second account holder have to be of legal age?

Yes. In a joint account, both account holders have to be of legal age.

Can I open a joint account with more than two persons?

A joint account always has two account holders. At the DKB, you can e.g. add up to four authorized persons, who will also get access to the online banking and/or cards. Some residential communities use the DKB for their residential community account.

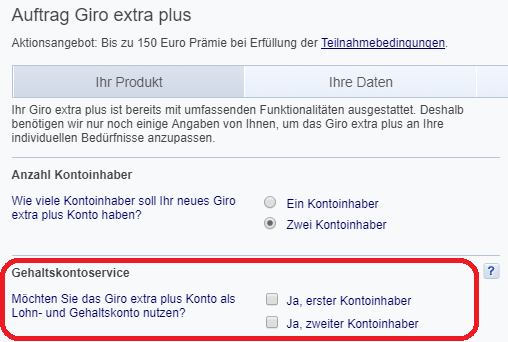

If you open the joint account at the Postbank, then only tick the “Gehaltskontoservice” (salary account service), if you are sure that you will arrange to change the salary payment to it. If you want to extensively test the account at first, then do not tick these boxes.

Do you have to legitimate together at the account opening?

The legitimating takes place separately. For example, the account holder 1 wants to immediately use the VideoIdent-procedure and account holder 2 will make the PostIdent in the subsequent days. Therefore, you can get legitimated in different places.

Does it matter who is account holder 1 or 2?

In the later use, it does not matter. Both account holders are equals.

As far as recognizable by you, it is recommended to state the creditworthiness-stronger partner as the account holder 1 at the account opening.

At the very end: How can you cancel a joint account?

For the cancellation of a joint account, the signatures of both account holders are necessary, at best in the same letter. If one of the two is no longer alive, then one has to add the death certificate.

Ready for the account opening?

Leave a Reply