ING-DiBa or Barclaycard Visa?

Sometimes, free credit cards are all placed under the same umbrella, although they are very different.

Which card is better suited for your individual use?

With this page, we give you a conclusive comparison, so that you know already before the card application with what you engage and what you can expect from the respective provider. At the end of this page, you will know how the land lies. 😉

| You can see the pictures of my own cards, because I use them myself and report of my own experiences. This is more authentic … |  ING DiBa |

Barclaycard |

| Annual fee | permanently free of charge! | |

| Opening of a connected current account? | yes (free of charge) |

no |

| Possible bonus / start balance | Euros 75 | Euros 25 |

| Application | ► online | ► online |

| Credit line | ||

| initial credit line (immediately after card application) |

Euros 0 up to 10,000 (very individual) Instruction |

Euros 500 up to 5,000 (very individual) |

| maximum credit line | Euros 10,000 (up to 3-times the proof of salary) |

Euros 10,000 (training program) |

| Can the credit line be increased through deposits? | yes | |

| Credit card payments | ||

| fee for payments in Euros | free of charge | |

| fee for payments in foreign currencies | 1.75 % of the transaction amount | 1.99 % of the transaction amount |

| Cash supply | ||

| Every ATM in Euros that accepts the Visa Card | free of charge | |

| Withdrawals in foreign currencies | 1.75 % of the transaction amount | 1.99 % of the transaction amount |

| Interest-free period | ||

| for card payments | 0–2 days (direct debit from the current account) |

up to 2 months (after the monthly billing another 28 days) |

| for cash withdrawals | ||

| Loan interest | ||

| … if one complies with all conditions cleverly … | 0 per cent | |

| regular loan interest | 6.99 % interest rate of the current account overdraft facility | 18.38 % from the day of card transaction (only at the use of the partial payment feature) |

| How can I avoid the loan interest? | having enough balance in the current account | transferring 100 % of card transactions until the due day (28th after the billing) or let it be debited automatically by SEPA-direct-debit |

| Service and extras for smart bank customers | ||

| Maestro-Card (former EC-card) | yes included free of charge! |

|

| Partner-card | yes free of charge at a joint account or power of attorney |

yes Euros 10 per year |

| Emergency service on journeys | no | yes emergency cash up to Euros 500 per day within 24 hours + replacement card within 3 days (free of charge!) |

| Telephone customer service | yes Mon–Sun around the clock |

yes Mon–Sun 8am–8pm, card blocking around the clock |

| Gold-card | – |  Who has transactions of Euros 3,000 or more per year with the card, could apply for the Gold-card immediately, because this is free in that case ► more information |

| Card application | ||

| Place of residence | Germany | Germany |

| Apply for the credit card: |  www.ing-diba.de |

www.barclaycard.de |

| Please give me your feedback through the comments feature about what card you decided for. Also the reason why. This way, we can better expand on the smart use (tips + tricks) in further articles. A heartly thanks for choosing DeutschesKonto.ORG for your research! |

||

Did you notice how different these cards are?

At some you might ask yourself, whether you can combine these cards meaningfully?

Yes! You can. But before you decide for it, please take a look at the tips and tricks of the use in the following paragraphs.

Tips and tricks for a smart use

What is the best about both providers?

That both are free of charge? Yes, but I did not talk about that. We at DeutschesKonto.ORG attach importance to that anyway.

You can get both cards with a credit line, without having to transfer the salary to them.

Both, ING-DiBa as well as the Barclaycard, are perfectly suited as a free extension – with charming features – to your existing current account! You do not have to change or cancel anything at your current financial management.

How do I get a high credit line?

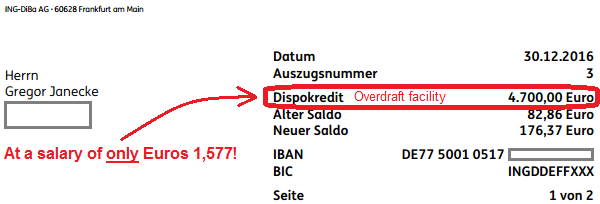

At the ING-DiBa, this is done through the proof of regular incomes. These could be transferred to the ING-DiBa-current account, but do not have to. How this works in detail, you can find out in this article ► Overdraft facility immediately at the account opening – also without salary transfer!.

The overdraft facility (= credit line of the Visa Card) is exactly at this amount since years.

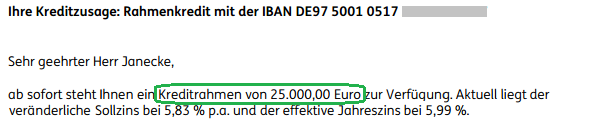

If Euros 10,000 – this is the highest possible credit line on the current account – are not enough, you can optionally book a 2nd overdraft facility (called credit line) up to Euros 25,000. No salary transfer is required either. The proof in the form of a pay slip is sufficient!

Additionally to the Euros 4,700, I got myself Euros 25,000 as a credit line. A credit line is like a second overdraft facility. But much cheaper!

The Barclaycard has its roots in Great Britain, which is why the setup of a credit line works different. A regular income is also a requirement, but you do not have to proof it. If you submit proof in the form of a copy of the last pay slip, then the initial credit line is usually higher.

For the setup of the initial credit line (between Euros 500 and 5,000), Barclaycard works together with the Schufa and the like. You need an average to good creditworthiness, so that your online application will be accepted.

After 6 months, the credit line automatically increases or you can ask for an increase. Important is that the card is actively used and that there were no payment difficulties.

How to train the credit card up to a limit of Euros 9,500, you can read in the report of the self-test here ► Instruction of how to increase the credit line.

I have trained my Barclaycard to a credit line of Euros 9,500. Even if I have not used the card for months, the credit line remained the same. Until today!

Credit line remains permanently generous!

How to avoid paying high credit card interest!

Right, nobody wants to permanently pay high credit card interest, this is why we have the description of how to avoid it:

-

ING-DiBa

Absolutely no loan interest applies, if you deposit money or just have it in the current account. At the ING-DiBa, the current account is at the same time the credit card account.

If you are in the red (you can let the account generally go into the red), then only the relatively cheap overdraft-interest of currently 6.99 per cent applies.

-

Barclaycard

Absolutely no loan interest applies, if you repay all credit card transactions until the due date. Herein, it is an interest-free period of almost 2 months (monthly billing + 28 days term of payment).

Advice: At the Barclaycard, you can submit a direct debiting, so that always exactly on the last day the full amount is debited from the current account (at your main bank). This way you ensure that you never pay loan interest!

If not the full amount is deposited/debited at the due date, then the partial payment feature is automatically activated. Little downside: The interest is charged retrospectively from the day of the actual transaction and the loan interest of Barclaycard is customarily-high for the credit card industry!

What should you do, if the credit card debt has become (too) much?

At Barclaycard, there is a monthly minimum-repayment of 2 per cent of the outstanding balance, but at least Euros 15. This regulation avoids that a possible mountain of credit card debt grows and grows. Given that you refrain from further borrowed payments!

Nevertheless, at an interest rate of more than 18 per cent, it is more difficult to repay the already made transactions. Per Euros 1,000, the interest debt is at Euros 14.16 per month.

Escape: If you are capable of paying a monthly installment of Euros 200 or more, then one can reschedule the debt at an interest rate of 4.9 to 8.9 % within the Barclaycard. This debt rescheduling, called payment plan, is very flexible and can be change or cancelled at any time. You can do this on your own in the online banking or let it be set up at the phone. Advantage: The interest rate is considerably lower and you repay the once created credit card debt much faster.

Better is of course that it does not come so far in the first place.

Please act responsible with credit cards and credit lines, just like we expect it from smart bank customers. But there are also situations in life, where you are super-happy, if you can immediately use an available credit line in an emergency! We have quite some people in our community, who faced such a case in the past and were glad that they could use a big balance over a period of time.

Experiences from the smart-bank-customer-community

Edi Grüner was the first person, who responded to my invitation of contributing something to this article. A heartely thanks!

Of course, I always try to only use the advantages:

-

The ING Visa is virtually immediately debited from the current account, which is good for not losing the overview of one’s expenses.

-

On the other side, there are also situations in which the very long term of payment of the Barclay is helpful.

-

When I e.g. pay something for others and I know that I get the money back soon (parents, friends or the company), I take advantage of the high credit line and up to 59 days terms of payment to not burden my private finances.

-

Neither can I complain of the service. After the acquaintance of my wallet with a big magnet, the two defect cards were replaced in an uncomplicated and fast manner. At the Barclay it was even free of charge.

Building big credit (card) lines

Even if you say today, “Well yes, Euros 300 overdraft facility of my Sparkasse are enough for me”, I want to motivate you to think about using offers of other banks and credit card companies and setting up one or two bigger overdraft facilities, because:

- you will become more independent from your main bank (some are at the mercy of their “consultant” for better or worse),

- you will become a more interesting customer, if you have 2 or 3 very good bank accounts,

- the probability is high that you increase your creditworthiness estimate at the Schufa and the like (at least me and many of our community have made this experience).

You are an interesting customer having 2–3 very good bank accounts!

Summary of the comparison

If the last paragraphs are not so important for you and you are just interested in an outstanding credit card that you can easily apply for online, then you get a brief summary of the comparison here:

| You see the pictures of my own cards, because I use them myself and report of my own experiences. This is more authentic … | ING DiBa |

Barclaycard |

| Annual fee | permanently free of charge! | |

| Opening of a connected current account? | yes (free of charge) |

no |

| Possible bonus / start balance | Euros 75 | Euros 25 |

| Initial credit line (immediately after card application) |

Euros 0 up to 10,000 (very individual) Instruction |

Euros 500 up to 5,000 (very individual) |

| maximum credit line | Euros 10,000 (up to 3-times the proof of salary) |

Euros 10,000 (training program) |

| Can the credit line be increased through deposits? | yes | |

| Withdrawing cash | free of charge in Euros at every ATM that accepts the Visa Card | |

| Interest-free periods | 0–2 days (direct debiting from the current account) |

up to 2 months (after the monthly billing another 28 days) |

| Apply for the credit card: |  www.ing-diba.de |

www.barclaycard.de |

| Please give me your feedback through the comments feature about which credit card you decided for. Please also the reason why. This way, we can better expand on the smart use (tips + tricks) in further articles. A heartly thanks for choosing DeutschesKonto.ORG for your research! |

||

Ready to start and apply for a card?

Very helpful article.

Still confused about the Barclay’s interest-free repayment period part.

Say, I use the credit card and at the end of the month I get a bill. Barclay will deduct 2% or 15€ automatically from my bank account on the billing day? Then I have 28 days to pay the rest of the sum?

If I add the direct debiting, when will Barclay deduct the amount; on the billing day or after 28 days of the billing?